Welcome to our official zero hour contract holiday pay calculator and resource guide. Before you calculate your leave, if you need to track your daily shifts, you can always use our free Weekly Work Hours Calculator on the homepage. Because your shifts change from week to week, applying the traditional "28 days a year" UK holiday rule simply doesn't work for your employment status.

How to calculate 0 contract hours holiday pay

For leave years starting on or after 1 April 2024, the UK government introduced a clear legal standard to resolve previous payroll disputes: your holiday now accrues directly based on the actual hours you work in a given pay period. The legal multiplier used for this is 12.07%.

What is holiday pay for zero hour contracts worth?

Essentially, the 12.07% statutory rule means that holiday pay for zero hour contracts accrues at a rate of just over 7 minutes of paid time off for every single hour you are on the clock. It is calculated by taking the statutory 5.6 weeks of holiday and dividing it by the remaining 46.4 working weeks of the year.

| Actual Hours Worked | Accrued Holiday Time (12.07%) | Rolled-up Pay Value (at £11.44/hr) |

|---|---|---|

| 10 Hours | 1.20 Hours | £13.81 |

| 25 Hours | 3.01 Hours | £34.52 |

| 40 Hours (Full Week Equivalent) | 4.82 Hours | £55.23 |

Getting holiday pay on a zero hour contract

A common source of confusion is figuring out exactly when and how the money is distributed. One of the biggest legal changes for workers getting holiday pay on a zero hour contract is the legal re-introduction of a system known as "Rolled-up holiday pay."

Instead of forcing you to keep track of accrued fractional hours and paying you only when you take a physical day off, your employer now has a more straightforward option. They can choose to process your distributions as an additional 12.07% supplement on top of your regular hourly rate in every single pay packet you receive. To learn more about broader worker rights, visit our UK Labor Laws Hub.

Rules for holiday pay 0 hour contract workers

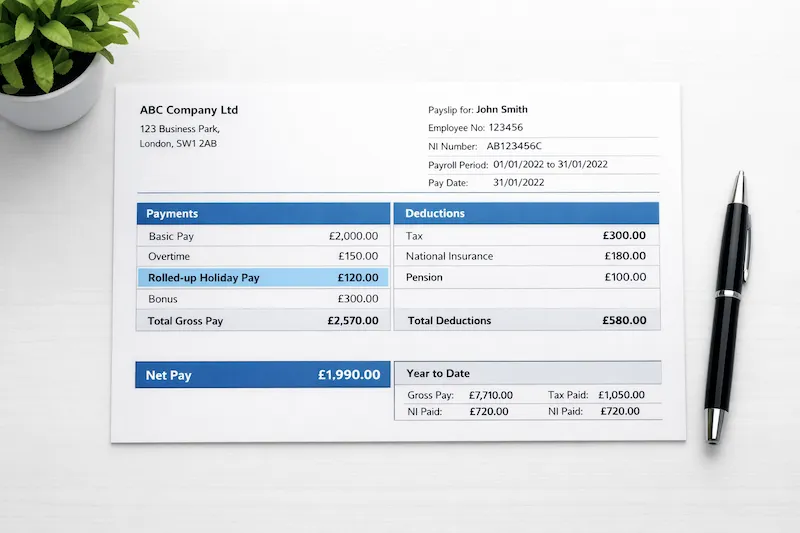

If your employer decides to use the rolled-up method for your holiday pay 0 hour contract earnings, they must adhere to strict HMRC transparency rules. The extra 12.07% cannot simply be hidden inside a vaguely "higher" hourly wage. Your payslip must clearly show the rolled-up holiday pay as a completely separate line item.

| Contract Type | Calculation Method | Can use "Rolled-up" Pay? |

|---|---|---|

| Zero Hours / Irregular Hours | 12.07% of actual hours worked | Yes, legally permitted as of April 2024 |

| Fixed Part-Time (e.g., set 3 days/week) | Standard 5.6 weeks rule (Pro-rata) | No, must be paid when time off is taken |

Understanding holiday pay zero hours contract taxes

Whether you choose to take the physical time off or receive the rolled-up pay supplement directly in your bank account, your holiday pay zero hours contract distributions are legally treated as standard taxable earnings. It is subject to standard Income Tax and National Insurance (NI) contributions just like your regular wages, and must be reported accurately to HMRC via the PAYE system by your employer.