Understanding Your HSE & Public Sector Pension

This calculator is specifically designed for the HSE Employee Superannuation Scheme (Standard Accrual). This model generally applies to nurses, administrators, and public sector staff who joined the Irish public service before 1 January 2013. If you need to convert your annual salary into an hourly rate to check your payslips, try our salary to hourly calculator.

PRSI Class A vs Class D: What's the Difference?

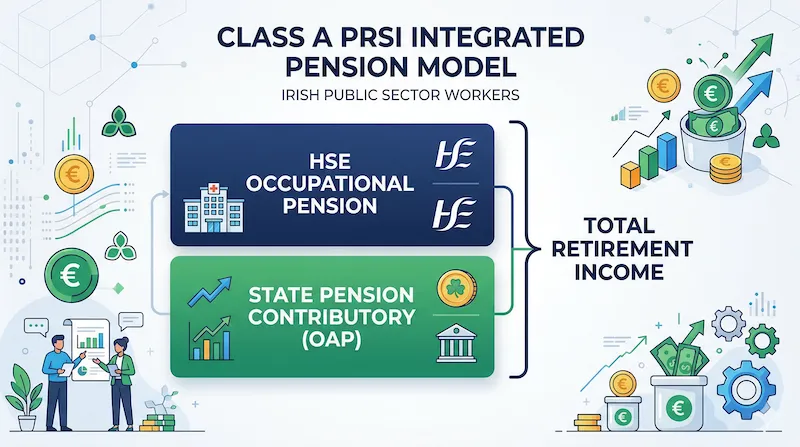

The most critical factor in calculating your retirement benefits in Ireland is your PRSI (Pay Related Social Insurance) Class. It dictates whether your HSE pension stands alone, or if it must be "integrated" (coordinated) with the State Pension.

| Feature | Class D (Pre-April 1995 Hires) | Class A (Post-April 1995 Hires) |

|---|---|---|

| State Pension Eligibility | No (Not entitled to full State Pension) | Yes (Entitled to State Pension Contributory) |

| HSE Pension Formula | Calculated at a flat 1/80th of final salary | "Integrated" calculation using a 1/200th base |

| Integration / Offset | None. You get the full HSE pension. | HSE pension is reduced to account for the State Pension you will receive. |

What if I joined the HSE after 2013 (Single Scheme)?

If you joined the Irish public service on or after 1 January 2013, you are a member of the Single Public Service Pension Scheme (SPSPS). This calculator will not work for you.

The Single Scheme abolished the "Final Salary" model. Instead, it uses a "Career Average" model. Every year, you build up referable amounts toward your pension and lump sum based on a percentage of your earnings for that specific year, which are then indexed to inflation (CPI). If your hours fluctuate week by week under the Single Scheme, tracking your base hours with a weekly time card is vital to ensure your annual accrual is recorded accurately by payroll.

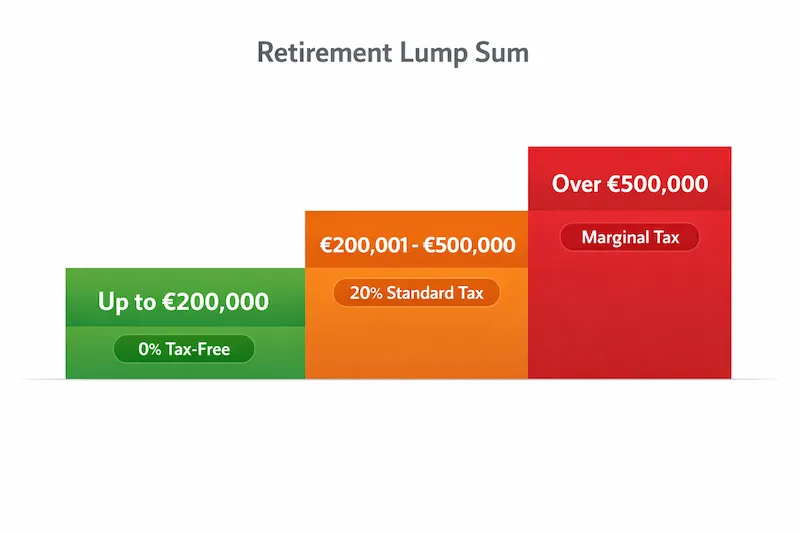

The Tax-Free Retirement Lump Sum Limit

Regardless of your PRSI class, pre-2013 standard accrual members are entitled to a retirement lump sum based on the formula: 3/80ths × Final Pensionable Salary × Years of Service (capped at 40 years, meaning a maximum of 1.5 times your final salary).

The Revenue Commissioners place strict limits on how much of this lump sum is tax-free in Ireland:

- Up to €200,000: Completely Tax-Free.

- From €200,001 to €500,000: Taxed at the standard rate (currently 20%).

- Over €500,000: Taxed at the marginal rate plus USC and PRSI.